Fintech Fran

Nubank Earnings

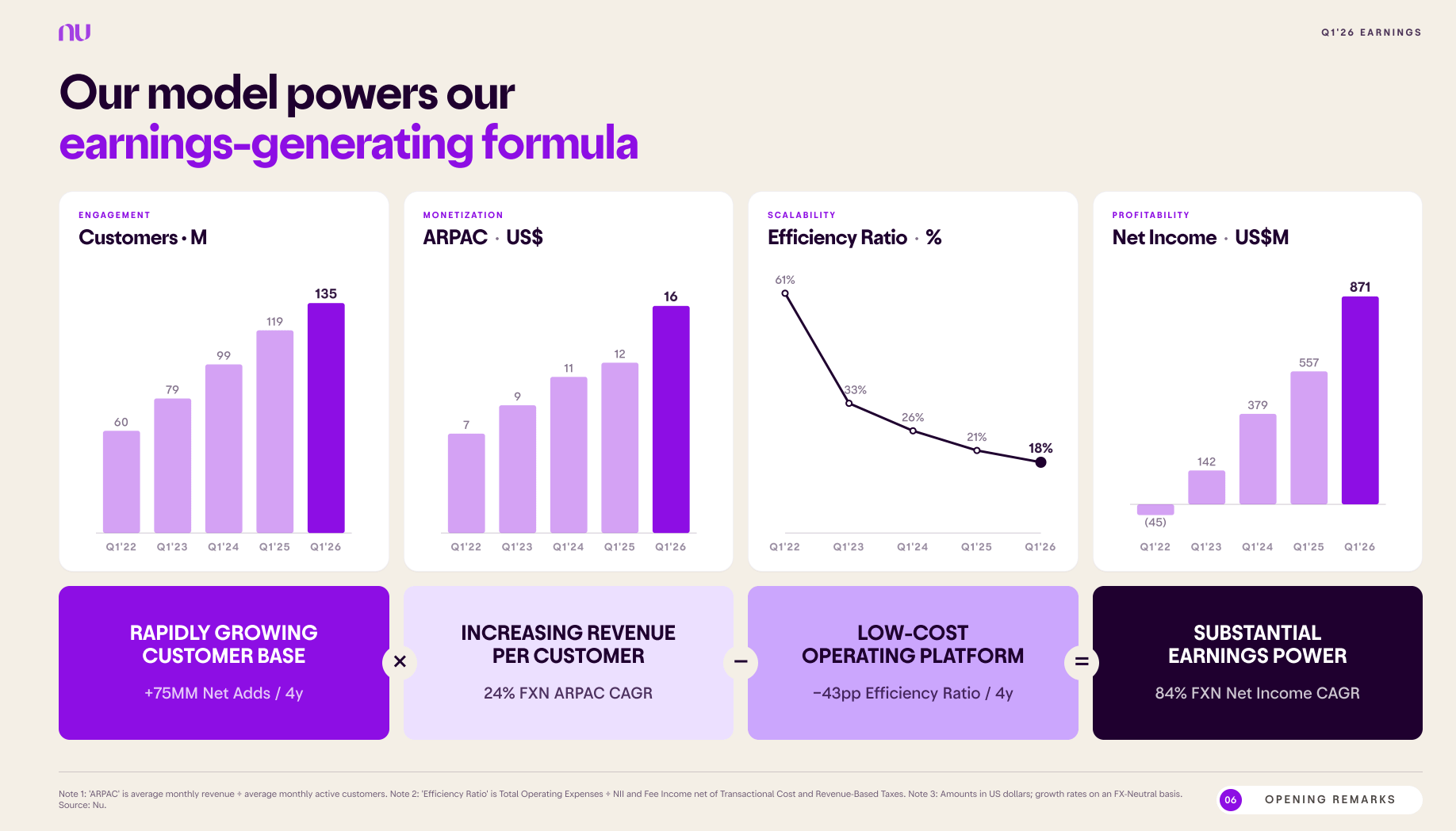

Nubank reported Q1 2026. They now have 135 million customers. Revenue passed $5B. Net income was $871 million.

But the story is Mexico. Nu crossed 15 million customers there. They are now the third largest bank in the country by users. They also reached break-even here.

Last month I wrote about Plata winning Mexico. But Nu has 15 million customers and a profit. I believe the market has room for more than one winner. Right now Nu is ahead.

The next test is the US. Nu got approval in January to start a bank. They want to open within 18 months. I am intrigued by this. Brazil and Mexico worked because banks were slow and people had no options. The US is not like that. People already have Chime and Cash App. The problem Nu solved back in Latam is not the problem here. Can they still win? I am not a 100% sure.

Fintech goes offline

Revolut is opening a store. It will be in Barcelona. It is not a bank branch. They call it an immersive space.

This is odd for a company built on an app. Revolut has 70 million customers and never needed a store. So why now? I think it’s because of trust. Revolut had a good year. Revenue was €5.2 billion, up 46%.

Capital One does this. They run cafés in many cities where you grab a coffee and sit down. You can ask about your account, but no one pushes you to.

Revolut is doing the same. The store is not there to sell. It is there to be seen. They will test it in Barcelona and copy it if it works. I think it is a smart and unique move. Revolut does not need stores to run. It needs them to grow its user base.

Trump Signs Two Fintech Orders

Last week Trump signed 2 executive orders that touch fintech. One helps. The other could hurt.

The first one opens doors. It tells regulators to cut rules that block new entrants. It asks the Fed to study whether non-banks can plug into its payment system. Today only banks can. A few things could shift. Bank charters get easier. This helps fintechs like Nubank that are already applying. Crypto and stablecoin firms get a path to move money without renting a bank.

The second one could hurt. It tells banks to tighten KYC on who opens accounts. It targets cross-border transfers used for crime. It tells lenders to treat possible deportation as a repayment risk. The reason given is fraud and security. But the effect could land on remittances. Money sent from US to Latin America is $174 billion per year. Some of the players here are Felix Pago, Western Union, and Remitly. If banks get stricter on who can send money, some of that flow gets harder and costs more.

The two orders pull in opposite ways. One wants fewer walls. The other wants tighter checks. Both ask. Neither forces. Now we wait and see how regulators react.

Fintech Rankings

I came across a fintech ranking that I found useful. It puts the incumbents and the newcomers side by side, so you can see the gap in one view.

By market cap, the old names still lead. Visa is worth $620 billion. Mastercard is $440 billion. American Express is $213 billion. These are the rails everyone uses. Years of scale put them far ahead.

Then come the new names. Robinhood is fourth at $66 billion. Nubank is fifth at $62 billion. Coinbase is sixth at $49 billion. These are the ones people talk about and the ones growing fast. But the gap is still wide.