Fintech Fran

Dystopian Fintech AI Future

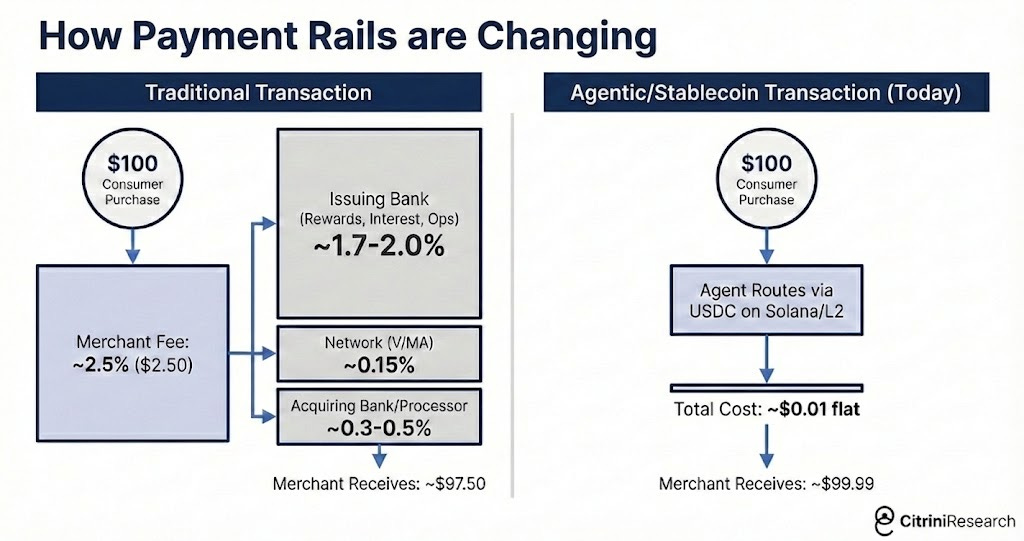

After reading a piece that went viral in the last few days on a dystopian AI future, I came to an idea that really impacted me on how I view the intersection of stablecoins and AI, in this case AI Agents. Imagine a (near) future where most online commerce is executed not by humans clicking buttons, but by AI agents transacting on our behalf.

In that world, the traditional card model starts to look inefficient. Today, when you spend $100 with a credit card, the merchant pays around 2–3% in interchange fees. That money funds rewards programs and profits for issuing banks, while networks and processors take their share. The system works because humans value credit, points, fraud protection, and convenience. But agents do not care about points. They optimize for speed, reliability, and lowest cost. If an agent can settle the same $100 transaction using stablecoins like USDC on Solana or an Ethereum L2 for fractions of a cent, avoiding the 2–3% fee becomes the rational default.

The real shift is not about crypto hype. It is about efficiency. If millions of AI agents begin routing payments through near-instant, low-cost rails, interchange becomes obsolete. Visa, Mastercard, and Amex that built entire business models around rewards funded by merchant subsidies could see pressure in their business model. I believe their moat was built on friction, meaning complex settlement, slow rails, and too many networks. If agents reduce that friction close to zero, the economics of payments could change in a world of agents.

Hyperscalers responsible for Fintech returns

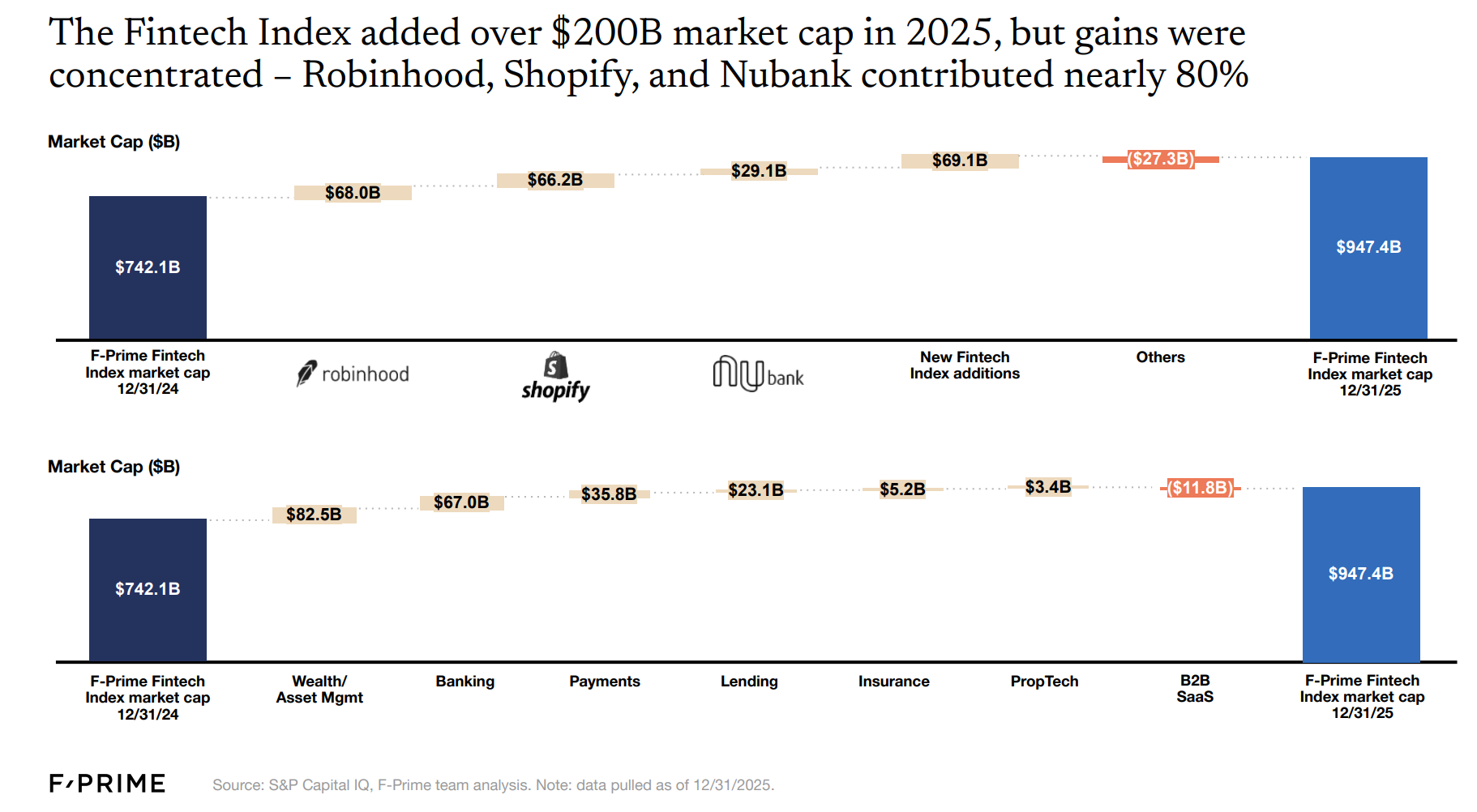

State of Fintech 2026 report by FPrime went out and one of the slides that caught my attention was that their index added market cap of $200B but that return was concentrated in a few Fintechs (the hyperscalers): Robinhood, Shopify, and Nubank,

In a nutshell, Fintech is bouncing back after 2021. The Fintech Index was up 60% for the year, though most gains came from a few big companies. IPOs and M&A are picking up again, but many new public companies are still below their IPO price. Investors now like steady growth and profits, not the bubble “growth at all costs.” Crypto had a big year, with stablecoins passing $1T in monthly volume and more ETFs launching. AI is getting lots of attention, but financial services is still adopting it slowly.

Robinhood democratizing access to pre-IPO companies

Robinhood made another great move by launching their first Ventures Fund to give its customers access to pre-IPO companies. It’s a $1B vehicle, with the typical 2% annual management fee. Companies in the fund include: Databricks, Mercor, Revolut, Ramp.

This is slowly giving everyone (people with a Robinhood account) access to pre-IPO companies that have always been a privilege reserved for accredited, sophisticated, and institutional investors.

It’s attractive as a user because there is no minimum investment, daily liquidity for customers, and no carry fees.

An amazing product, in my opinion.

Stripe Annual Letter

Stripe annual letter just came out. Stripe is clearly becoming core infrastructure for the internet economy. In 2025, businesses on Stripe processed $1.9T in payments (Mexico GDP), about 1.6% of global GDP. It now powers millions of companies, including 90% of the Dow, 80% of the Nasdaq 100, and 25% of new Delaware corporations.

The new wave is even more impressive. The 2025 customer cohort is Stripe’s strongest ever, growing much faster than last year’s. More companies are hitting $10M ARR within months of launch, and more Atlas startups are charging customers within 30 days. Stripe Capital also helps businesses grow meaningfully faster. And with AI companies building and monetizing from day one, Stripe is becoming the default payments layer for the AI economy.

Stripe’s valuation just jumped to $159B from $92B in 12 months through a new employee share sale. And still, an IPO isn’t even a top priority. Can Stripe keep growing? In my opinion definitely yes, especially with the intersection of finance and AI.